Protecting your home, car, and business with insurance is a smart idea. Insurance coverage is designed to safeguard the investment you have made in your property and business. But when unexpected risks over and above standard insurance liability coverage threaten your finances, another type of coverage can make a big difference. Umbrella insurance is designed to pick up when the liability coverage on your other policies is exhausted.

In this article, we’ll explain how umbrella insurance works, what it does and does not cover, coverage options, and how to save on costs. You’ll also learn how an independent insurance agent can help you anticipate legal risks ahead of time and choose the best umbrella coverage for your peace of mind.

What Is Umbrella Insurance?

Umbrella insurance, also called excess liability coverage, is a separate insurance policy that acts as a liability “umbrella” that provides extra coverage protection for your business, auto, home, motorcycle, and boat policies. It’s a liability-only policy, meaning it can help cover costs if you are sued for injuries, property damage, or personal actions that cause mental anguish or harm to another person’s reputation. Umbrella insurance simply extends your underlying policy's liability limits in the event of a large claim.

Most insurance companies offer umbrella policies in million-dollar increments, starting at $1 million and ending at $5 million. However, some offer a lower limit, like $500,000, or even a higher limit, over $5 million. When you speak to your independent agent, they'll be able to guide you to what's best for you and handle all the heavy work to find it for you.

How Does Umbrella Insurance Work?

Umbrella insurance expands a policy’s liability coverage to help cover the costs of lawsuits, settlements, and legal defense, as long as the reason for the lawsuit is covered by your policy. If you have a party at your house and a guest trips on the uneven pavement leading to your entry, they could sue you for medical and legal expenses, lost wages, and more. If they are awarded $200,000 in damages and your homeowners insurance covers you for up to $100,000, your umbrella coverage can help cover the additional costs of your legal defense and settlement.

Umbrella insurance can even sometimes cover certain types of lawsuits that aren't covered by your homeowners, business, or auto insurance – such as libel, slander, or invasion of privacy.

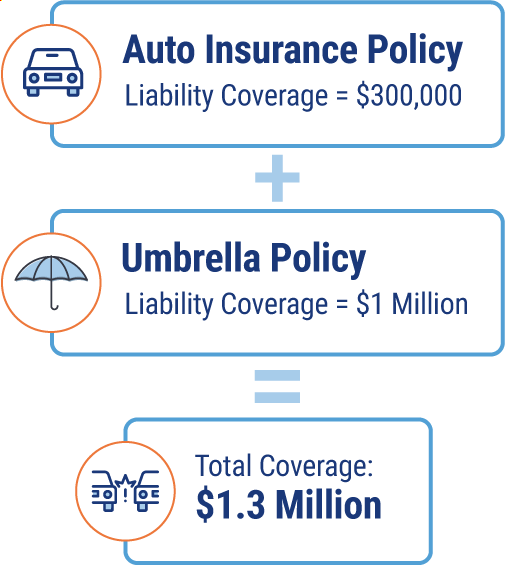

Here's a breakdown of umbrella coverage on top of an auto insurance policy:

So, if you had an auto insurance policy that provided $300,000 in liability coverage and then added a $1 million umbrella policy, you'd have increased your liability protection up to $1.3 million total. The good news is that umbrella policies tend to be highly affordable. Especially considering the generous amount of added protection they offer.

UMBRELLA INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

What Does Umbrella Insurance Cover?

An umbrella policy is designed to extend liability protection included in other types of insurance. Personal umbrella policies are most commonly paired with homeowners insurance, auto insurance, or watercraft insurance. Conversely, business umbrella policies are paired with general liability coverage under business insurance or commercial auto insurance.

Just as a regular umbrella protects you against harsh weather, umbrella insurance protects you against harsh legal consequences. In addition, umbrella coverage can extend to other members of your household who do not have car or property insurance in their own names. Generally, umbrella insurance provides liability coverage for expenses and lawsuits for covered claims involving:

Personal injury to others

Damage to other people’s property

Claims of libel, slander, defamation of character, or invasion of privacy

Landlord liability

Umbrella insurance usually covers:

Umbrella insurance usually doesn’t cover:

Others’ treatment for injury and funeral costs

Your own injuries

Others’ property damage

Damage to your personal belongings

Lawsuits involving slander, libel, defamation of character and other personal attacks

Others’ injuries or property damage that your business is liable for

Your legal defense costs

Intentional or criminal acts

What Doesn't Umbrella Insurance Cover?

Umbrella policies aren’t standard across the country. This means your policy could look quite different from your neighbor's. In addition, umbrella coverage does not cover expenses if:

Damage happens to your own property.

You intentionally harm someone or engage in illegal activity.

Claims are not covered by your primary policy or specifically excluded by your primary or umbrella policy.

You have a contract that makes you liable for the safety of workers on your property.

Umbrella policies come with a “self-insured retention,” which is similar to a deductible. The policy will spell out how much you have to pay before your umbrella coverage will pay on a claim.

It’s important to understand that personal umbrella insurance will not cover losses from your business operations. For that type of coverage, you’ll need commercial insurance.

Sound complex? One of the primary roles of an independent insurance agent is to understand your needs for umbrella coverage, explain your options, and ensure you understand what is and is not covered.

Do I Need Umbrella Insurance?

Umbrella Insurance Pros:

Umbrella Insurance Cons:

Provides extra liability coverage and legal defense costs once the limits of your auto, home or business insurance have been exhausted.

You must already carry auto or property insurance, usually homeowners, to qualify.

Covers incidents your primary insurance may not, like libel and slander.

You're required to buy a minimum amount of auto and/or property insurance liability coverage before you can add umbrella coverage.

Your umbrella policy is there to help protect your finances against unforeseen, expensive legal troubles. Here are a couple of common scenarios where umbrella insurance is critical.

Car accidents: Whether you hurt someone else with your vehicle or damage their property, lawsuits following car accidents can quickly exceed your standard auto coverage.

Dog bites: Dog bites can be some of the most expensive legal claims filed against homeowners, with an average cost in one recent year of $49,025.

Guest or customer injuries: Accidents on floors, stairs, and sidewalks are common and can result in costly lawsuits when filed against homeowners and businesses. Without additional protection, your finances could take a big hit.

How Much Umbrella Insurance Do You Need?

To decide how much umbrella insurance coverage you need, it helps to understand the value of all of your assets. The more you have, the more you stand to lose. So, if the value of all your property, savings, and investments adds up to $2 million and your current insurance policies cover liability up to $1 million, you’ll have a gap of $1 million. That gap represents how much umbrella coverage you should have.

Umbrella insurance is typically sold in increments of $1 million. You may think that is a lot of money, but lawsuits can quickly add up to amounts greater than that. Remember, umbrella coverage is designed to protect your finances. How long would it take you to recover from having to pay $1 million or more out of your own pocket?

There is no law requiring you to have umbrella insurance, but it can be a good idea. For many people, $1 million in umbrella coverage can equal great peace of mind. But in situations like these, you may want more than $1 million in coverage:

You have an inexperienced driver in your family.

You coach kids’ sports or serve on a volunteer or nonprofit board.

You own more than one property and/or are a landlord.

You own things that could result in injury to others (pool, trampoline, guns, a dog).

You are a public figure.

You own a business.

How Can Umbrella Insurance Help Protect You?

Umbrella insurance protects your finances from unexpected events that result in you being held responsible for damages or injuries to others. When those events happen and costs exceed your standard insurance coverage limits, umbrella insurance is there to help cover the costs and prevent your financial ruin. Here are some examples:

Your dog bites a visitor: While homeowners insurance can help cover expenses associated with injuries caused by your dog, the costs or your visitor’s lawsuit may be higher than what is provided by your coverage. Umbrella insurance can help cover those costs or if you are found legally responsible.

You accidentally crash your car: It happens. You (or your inexperienced teen driver) hit the gas instead of the brake. The car crashes into a storefront or another car. The resulting damage can add up fast, especially if those affected by the crash decide to sue you. While your auto insurance will pay first, your umbrella policy can stand in the gap to manage the additional costs.

Your kid’s social media post creates backlash: When your kid posts some teasing remarks on his social media account about another child, that child’s parents may choose to sue you for libel, pain, and suffering. Even if the suit is decided in your favor, you will still incur court costs. Your homeowner’s policy may partially cover those costs, while umbrella insurance can cover the remainder.

How Much Does an Umbrella Policy Cost?

Most insurance companies offer $1 million umbrella policies priced around $200 per year. For an additional $1 million dollars in coverage, you'd add about $100 to your annual premium and about another $75 per year for each additional increment of $1 million. Costs will vary, depending on the amount of coverage you choose and other risk factors.

A driving record with accidents or violations in the last three to five years

How To Purchase an Umbrella Insurance Policy

To purchase umbrella coverage, you will need to do so through the same company that provides your home, auto, renters, or business insurance. According to the Insurance Information Institute, you will usually need to have $250,000 of liability insurance on your auto policy and $300,000 of liability insurance on your homeowners policy before umbrella insurance can be added.

Your independent agent can help you review your options for umbrella insurance. When you are ready to add umbrella insurance, you will need to provide:

Your auto or homeowners insurance policy information, including liability coverage amounts

Driving history for all members of the household

Names of all vehicle owners

Information about any additional properties that you own, including insurance coverage on those properties

History of liability claims

History of civil or criminal charges

Umbrella Insurance FAQ Answered

Simply put, personal umbrella insurance pairs with family policies like home, auto, or boat insurance. Business or commercial umbrella insurance pairs with your business's general liability or commercial auto insurance.

Unless you can predict the future, you really never know if you need umbrella insurance. However, if you're exposed to a large number of liability risks, it's definitely an important coverage to consider. If your home has potentially dangerous hazards, or your speed boat loves to chop up the waters, then umbrella insurance is probably a good idea.

The extra padding of liability protection will always help you sleep at night, and if something unexpected ever happens, it can help minimize the financial damage to you and your family.

When thinking about umbrella insurance coverage, consider the value of your assets (your property, savings, and investments). If that value adds up to $2 million, and your current insurance policies cover liability up to $1 million, you’ll have a gap of $1 million. That gap represents how much umbrella coverage you probably should have.

Since you never know what could possibly happen tomorrow, your best option for determining your coverage is to work with an independent insurance agent. They'll be able to help assess your situation and all risks associated with your life to lay out the best coverage options for you.

Many families find the popular $1 million in additional liability coverage more than enough, while others will require much more.

No. Natural disasters relate to property damage, not liability, and umbrella insurance only focuses on that side of protection. If you do need natural disaster property coverage, your independent agent can work with you to find the best course of action.

Your umbrella insurance is an extra buffer of coverage on top of the policy it corresponds to. If you're in a car accident, your auto insurance liability coverage will protect you up to the limits of your coverage. Umbrella insurance will kick in on top of that to help cover the costs if you are sued for causing injuries to others or damage to property.

As far as the action steps you take after an incident, you'll simply file a claim. The insurance company will hire an attorney on your behalf and pay for the cost of the litigation, including settlement up to the limits of the policy.

Yes, umbrella insurance can be paired with rental property insurance for landlords. This is definitely a good idea if you operate a larger rental unit with multiple families and tenants involved. Your umbrella coverage will be attached to your landlord insurance and liability protection.

Umbrella coverage increases liability coverage limits to protect your finances in the event you are sued for injuries, property damage, or personal actions that cause mental anguish or harm to another person’s reputation. If your property is damaged by fire, vandalism, floods, or other causes, you’ll need separate coverages.

Umbrella insurance can be a great value for its cost. It can deliver you peace of mind if an unexpected event happens and you are sued for financial damages. With umbrella insurance, your finances are protected.

Your Independent Insurance Agent Has Your Answers to Umbrella Insurance Questions

Whatever you need, your agent has your back. With a brief intro into the terms, discounts, and process of your umbrella insurance, you now know the kinds of questions to be asking. Your agent will ask you all about your liability needs and goals to help find the perfect blend of coverage at the right cost for you.

Best Umbrella Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What our customers are saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.