Get professional liability insurance coverage options and quotes.

March 4, 2025

How will this quote help me?

Your quote is based on several common factors to give you a clear picture of the cost you can expect for professional liability insurance, though an independent insurance agent can shop around and maybe even improve your rate!

NOTE: This quote is not final, though we did work with professional actuaries to help get you a ballpark figure to get started.

PROFESSIONAL LIABILITY INSURANCE

Find the perfect agent to shop multiple insurance companies on your behalf, saving you time and money.

A professional liability insurance policy offers businesses the protection they need against third-party claims of misrepresentation, negligence, inaccurate advice, and other incidents that lead to a form of injury or loss. Claims can be made against a business or professional individual by customers, clients, or the public. Any business or professional with a risk of facing a lawsuit from a third party for negligence and other related claims should consider getting professional liability coverage. These policies provide reimbursement for third-party damages after a service you performed incorrectly or one you failed to perform at all. An independent insurance agent can help you save money on professional liability insurance and help you find the right type of policy for your needs by comparing quotes from multiple carriers.

What Is Professional Liability Insurance?

Simply put, professional liability insurance is a form of business coverage designed to protect professionals against liability costs resulting from errors or omissions in the services they provide.

It's important to understand that in nearly every profession, customers and clients can—and will—sue if the job you did for them doesn't meet their standards. And if you're caught without coverage, you’ll have to pay some pretty expensive legal defense costs out of pocket, enough to potentially ruin your career goals.

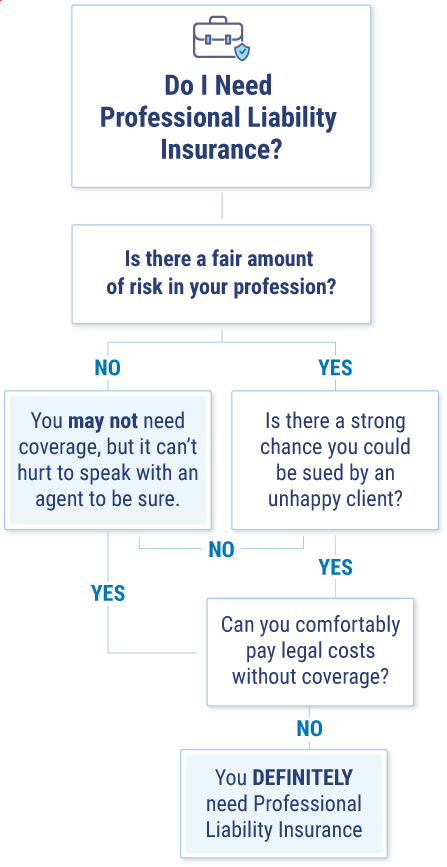

Why Do I Need Professional Liability Insurance?

If you work for a large company, firm, or clinic, you probably already have existing general liability coverage, maybe even professional liability as well. But that coverage has limits and may not be enough to protect you.

No matter how experienced you are, accidents can happen. Sometimes even the slightest mistake can lead to some significant financial damage to your client's business. In such instances, you can often expect a lawsuit to follow.

Any lawsuit, whether it gets settled in or out of court, is likely to be expensive to resolve. Professional liability insurance is designed to help protect you from what could otherwise be a serious financial burden.

If you work in a legal or medical field, malpractice insurance is critical. Malpractice coverage is professional liability insurance for legal and medical professionals.

What Is E&O Insurance?

Errors & omissions insurance, also called E&O insurance, is just another name for professional liability insurance. The two terms are used interchangeably to refer to coverage that protects businesses and professionals against errors that occur on the job and cause alleged harm to customers or clients. Depending on the specific insurance company you select, you might find they call their professional liability coverage E&O insurance.

What Does Professional Liability Insurance Cover?

There are a couple of different types of professional liability policies based on what you do in your line of business and provide to customers or clients.

Professional liability coverage is designed for those who provide advice or other related services to the public, like lawyers, consultants, insurance agents, and architects. It protects against lawsuits that claim a financial loss occurred based on bad information or negligent advice.

E&O Coverage Levels

Covered

Not Covered

Mistakes made at work

Services not performed

Breach of contract

Missing contract deadlines

Professional negligence

Occurrence/Tail

General liability

Workers' compensation

Commercial property

Employment practices liability

Commercial auto

List of Features Covered by Insurance

Lawsuits are common in most professional industries, and finding the right liability coverage starts with understanding the two distinct types of policies available.

A claims-made policy must be in effect both when the lawsuit is filed and when the incident in the suit took place. This policy type is the most common and is usually less expensive.

An occurrence policy covers any incident that takes place during the coverage period, even if the actual lawsuit is filed after the policy expiration. This type of policy provides more comprehensive coverage and is often more expensive.

An independent insurance agent can help answer any questions you may have about your liability needs, coverage, and other specifics and can help steer you toward the right protection for your profession.

What Does Professional Liability Insurance NOT Cover?

Remember that professional liability insurance doesn’t cover everything. It won’t help your business with these kinds of claims:

Bodily injury or property damage: You’ll want to get a general liability insurance policy to help cover your costs if someone gets injured on your business premises or if you damage another's property and the incidents are unrelated to professional activities. Professional liability will cover these incidents only if they result from faulty professional advice or services.

Work-related injuries or illnesses: If your employees get hurt or sick due to their job, you’ll need workers’ compensation insurance to help them recover and return to work.

Data breach: You’ll need cyber liability insurance if your business handles confidential or sensitive client transactions, including personal information like email addresses and passwords or financial records like banking account info, etc.

Your independent insurance agent can further explain the exclusions in professional liability insurance and help get you set up with the other types of coverage you may need.

What Are the Requirements for Professional Liability Insurance?

Some jobs require business professionals to have professional liability insurance, though they may also need additional coverage and other forms of business insurance, too. Professionals who work as doctors, lawyers, financial planners, insurance agents, therapists, church counselors, and wedding planners are typically required to have professional liability insurance before they can take on clients or customers. In any case, if you perform a type of work that requires a contract between you or your business and clients or customers, or otherwise offer professional advice or services to the public, you'd benefit from having a professional liability insurance or E&O policy.

How Much Professional Liability Insurance Do I Need?

The best way to determine the amount of professional liability coverage your business needs is to speak with an independent insurance agent. Together with you, they'll get to know your business needs and help determine what's right for you. But in general, there are a few commonly big factors in determining your coverage needs.

Business size: How big is your business? What are your sales? How many customer interactions do you have on a daily basis? A larger company will need more liability protection.

Number of employees: Do you run a sole proprietorship? Have a larger business? The more employees, the larger the possibility for mistakes and lawsuits and the more coverage you'll need.

Business location: Where you deal with your customers matters. The larger the risk, the more protection you'll want to have in place.

Services provided: Different services come with different risks. Each profession has its own risk level and needs for a certain amount of coverage.

No need to memorize these questions, as your independent insurance agent knows exactly what to ask and look for when determining how much E&O insurance you need.

How Much Does Professional Liability Insurance Cost?

When it comes to insurance, the pricing system is generally very simple. The more risk involved, the higher the insurance premiums must be. A policy for a neurosurgeon or anesthesiologist will be more expensive than a policy for, say, an independent insurance agent.

To get exact pricing specific to your profession, speak with a local independent insurance agent. They'll be able to help you find the proper blend of coverage and cost.

Frequently Asked Questions about Professional Liability Insurance

Any professional who operates their own business or provides a service to customers, clients, or the public should protect themselves with professional liability insurance. This coverage protects the insured against the hefty financial loss that can come with lawsuits filed against them by their clients.

If something goes wrong and you damage someone or some business financially, the legal fees can be catastrophic to an individual. Any lawsuit, whether it ends up in court or is settled without it, will be expensive to resolve. Professional liability insurance is designed to help protect you from what could be a serious financial burden.

Think of professional liability insurance as coverage that protects you from client lawsuits after financial damage or loss, whether that's from things you did as a part of your contract, or things you neglected to do that may have led to harm. If you're caught without coverage, you’ll have to pay some pretty expensive legal defense costs out of pocket.

Within professional liability insurance are unique policies like errors & omissions insurance and malpractice insurance. Errors & omissions is designed to protect professionals who provide services, like consultants, accountants, etc., whereas malpractice is designed to cover medical and legal professionals.

There are two different professional liability coverage types: a claims-made and an occurrence policy.

A claims-made policy must be in effect both when the lawsuit is filed and when the incident in the suit took place. This type of policy is the most common and is usually less expensive.

An occurrence policy covers any incident that takes place during the coverage period, even if the actual lawsuit is filed after the policy expiration. This type of policy provides more comprehensive coverage and is higher priced.

Errors and omissions liability insurance, also called E&O insurance, is a form of professional liability coverage. E&O insurance was designed for those who provide advice or services like consultants, insurance agents, and architects. It protects against lawsuits that claim a financial loss occurred based on bad information or negligent advice.

Malpractice insurance is a form of professional liability coverage. This specific form of insurance was designed for medical and legal professionals like psychiatrists, podiatrists, and gynecologists. It protects against lawsuits that allege negligence or mistakes. If you work in the healthcare industry, malpractice insurance is an absolute must.

It depends. In most cases, whether you work for a hospital, a law firm, or an insurance brokerage, you should be protected under your employer's professional liability coverage. However, that policy has limits. If a claim has already been made against the policy, the company's coverage limit may have already been reached.

Beyond that, your employer is most concerned with their own coverage, which may leave gaps in the protection that's more important to you. Speak with your employer and your independent agent to ensure that you have the right coverage for your needs.

No matter what you do for a living, there are risks associated with it. The more risk involved, the higher the insurance premiums are likely to be for whatever type of coverage you need. It's hard to offer a ballpark figure for a professional liability policy without knowing more about the risks you face.

To get exact pricing specific to your profession, speak with an independent insurance agent. They'll help you find the right coverage and policy at the perfect cost for your budget.

With access to multiple insurance companies, independent insurance agents are unlike any other type of agent out there. They’ll help find you the best coverage options and most competitive prices, all for free.

Your Independent Insurance Agent Has Your Answers for All Questions about Professional Liability Coverage

Whatever you need, your independent insurance agent has got you covered. With a brief intro into the terms, discounts, and process of your professional liability insurance, you now know the kinds of questions to be asking. Your agent will ask you all about your line of work, its risks, and your goals, and will help find the perfect blend of coverage and cost for you.

Best Professional Liability Insurance Companies

More Choices

Our independent insurance agents work for you, not the insurance companies. That means you always get the best coverage options to choose from.

Better Prices

When you have options from multiple companies, it's easier to find the best coverage at the right price, at no extra cost to you.

Local Services

There's an independent agent in every city who always understands the insurance coverage you need most based on local laws and needs that apply to you.

What Our Customers Are Saying

Work Done For Me

I looked at different individual companies, but it was so time-consuming to fill out each individual application and keep track of them all. Trusted Choice got back to me quickly and gave me an option that worked. I ended up with Travelers, which has a great price. The online process was pretty easy. Plus, they did the legwork for me. It was a great experience.

June of Medina, NY

Multiple Options

I tried finding insurance myself but I wasn't coming up with very much. I contacted Trusted Choice and they looked at various options and presented it to me. Everything with the agent went very smoothly... He knew exactly what we wanted and searched accordingly. I was able to choose the one that I thought was best so it worked out for me. I'm happy that I did it that way.

Dean of Loveland, CO

So Easy

I needed insurance for the home that I was buying and based on the pricing, I went with Trusted Choice. The process was all done online and I didn't really have to do too much. The website was also easy to use and navigate and it was not overly intimidating. Everybody that I've dealt with also seemed good and professional. It was a positive experience.

Jacob of Mesa, AZ

One-On-One Attention

Every year I search for insurance to make sure that I’m getting the best bang for my dollar. I went with an independent agent because if I go through them, I get that one-on-one instead of being just a number.... The experience was great.

Rudy of Altamonte Springs, FL

Really Helpful

TrustedChoice.com was real helpful when I needed to get insurance. The agent gave me the basics of what I'd be getting if I got insurance with them.

Christine of Chipley, FL

Multiple Agents

I needed a different independent agent to get insurance and I went with Trusted Choice. Their website was helpful in connecting me to two or three other agents that I was able to speak to. Their site did what I needed.

George of North Haven, CT

More Coverage

Trusted Choice's online process is super easy. They pulled most of the information and I ended up going with one of their recommendations. Aside from them, everybody else was too expensive. Plus, the Trusted Choice agent offered more coverage.

Kirstin of Colorado Springs, CO

Great Match

Everybody at TrustedChoice.com was helpful and pleasant. They set us up with a great match and gave us our best option and price.

Tawny of Hubert, NC

Best Coverage and Rates

I did a lot of searching for insurance and I went with a Trusted Choice agent because they provided the best rates and coverage. I haven't had a claim but I know I'm covered and that's good news. I would recommend Trusted Choice.